-

Key Takeaways

-

Drone Market Snapshot 2026

- Commercial vs Recreational

- Regional Leaders

- High-Growth Niches

-

Regulation & Airspace Integration

- United States – Part 108

- United States – UTM Systems Mature

- Global Moves

- United States – FCC Drone Bans

- 2026 Compliance Checklist

-

Technology Accelerators

- AI-Powered Autonomy

- BVLOS & Detect-and-Avoid

- Sensor & Payload Revolution

-

Industry Adoption Trends

- Energy & Utilities (14.5% CAGR)

- Logistics & Delivery

- Agriculture & Environmental

- Construction & Infrastructure

- Public Safety & Defense

- Media, Survey, Insurance

-

Business Models & Economics

- Drone-as-a-Service (DaaS)

- Workforce & Skills Gap

-

Security, Privacy & Counter-UAS

- U.S. Drone Makers Seek Asian Markets

- Counter-UAS (CUAS) Market Growth

- Data Governance

-

Challenges & Risk Factors

-

Beyond 2026 – Future Trends to Look For

- Swarming & Collaborative UAS

- Hydrogen & Hybrid-eVTOL Cargo

-

Market Projection Chart

-

Conclusion

Think back to 2016, when pilots fought for line-of-sight waivers. Would you have ever dreamed that just a decade later, autonomous drones could fly well beyond visual line of sight for hours?

In 2026, businesses and governments alike are expanding drone operations, creating unprecedented opportunities and challenges.

In this article, we explore the latest industry trends shaping the drone market. It’s time to get ready for Part 108 and what the next wave of aerial technology will mean for industries worldwide.

Get Your FREE Drone Sticker

Stop using masking tape.

Add a pro label in minutes.

- Fits on drone arms.

- Clean, readable format.

- Free, mailed to you.

- Ships in ~7–10 days.

Key Takeaways

- Stay up to date with the latest market developments.

- Explore regulatory changes and the coming of Part 108 BVLOS rules.

- Learn what you need to stay compliant in 2026.

- Discover the innovative, cutting-edge technologies driving market growth.

- Pinpoint key industry trends in top sectors like Energy & Utilities, Cargo & Logistics, and Defense.

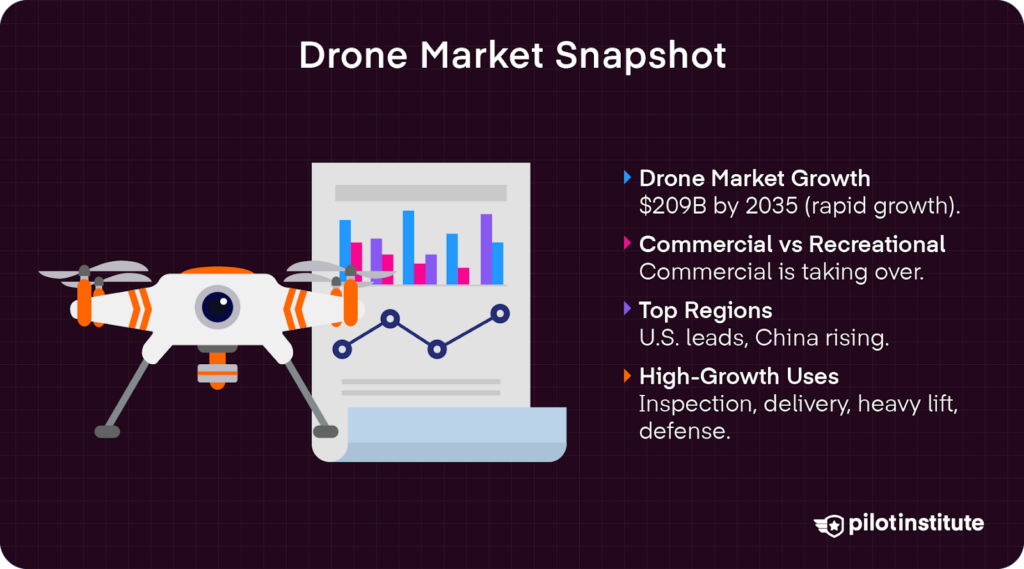

Drone Market Snapshot 2026

Drone market segments continue to witness unprecedented growth in 2026. From 2026 to 2035, the drone market size is expected to increase by 16.77% compound annual growth rate (CAGR), reaching an impressive $209.91 billion in 2035.

This surge represents more than industry expansion. It is a prime opportunity for entrepreneurs, operators, and investors to enter a high-growth market that is reshaping our skies.

Commercial vs Recreational

Personal drones flown recreationally are categorized under a consumer market. According to a report by Persistence Market Research, the global consumer market size is expected to reach a value of $6.3 billion in 2026, hitting a staggering $14 billion by 2033.

Advances in camera technologies continue to drive interest in the consumer drone market. Recreational pilots are flocking to affordable aerial photography drones such as the DJI Air 3S. FPV drones are also more accessible, fueling demand for smaller, lightweight drones that can still handle rugged use.

Yet, the recreational market is expected to contract in several regions, thanks to lagging economic growth and reduced consumer spending.

In fact, the commercial market is poised to overtake the recreational one, growing at 8.3% annually. There has been a major uptick in commercial applications, which Business Wire described as “particularly robust momentum.”

Regional Leaders

North America held 37% of the market share in 2025. In the U.S., the drone industry is expected to see a 13% CAGR from 2025 to 2030, reaching a market size of $163.6 billion at the end of that period.

Yet, there has been impressive growth in other markets, led by a 14.8% CAGR expected in China from 2025 to 2030. In 2023, there were over 2 million drones registered with the Civil Aviation Administration of China. Demand in China is driven largely by agricultural and military applications.

Infrastructure inspection needs are also driving demand in emerging markets in the Middle East and Africa. These markets are expected to grow to $7.65 billion by 2031, an impressive increase from the expected $2.6 billion market size seen in 2026.

High-Growth Niches

A Drone Industry Insights report highlighted the energy industry as experiencing the highest increase in demand for drones. Utility providers increasingly rely on unmanned aircraft for infrastructure inspection and assessment to improve safety and reduce costs.

This was followed by high growth in cargo and delivery services. For example, Wing is expanding its autonomous delivery networks, scaling ecommerce drone delivery for top retailers including Walmart.

Heavy lifting is also a key driver of growth. Advances in payload capabilities empower drones to carry heavier loads, meeting commercial demands in industries like construction, agriculture, and utilities.

In fact, drones carrying up to 330 lbs (150 kg) represented the largest market segment in 2025. Those carrying up to 1,323 lbs (600 kg) are now expected to have the fastest growth from 2026 to 2035.

A global uptick in defense spending is also pushing high-end market acceleration. Governments are investing heavily in UAS for surveillance, reconnaissance, tactical operations, and emergency services.

Regulation & Airspace Integration

United States – Part 108

The U.S. is facing a massive overhaul of its beyond visual line of sight (BVLOS) regulations with the coming of Part 108.

The FAA released its Proposed Rule in 2025 for normalizing automated autonomous BVLOS drone operations in U.S. airspace. Part 108 provides a framework to incorporate large-scale BVLOS operations with minimal human supervision.

It replaces the headache of applying for Part 107 waivers, instead offering a simple, scalable pathway for routine BVLOS flights.

Part 108 has several key requirements. First, you’ll need a special certification to operate, called an operator-in-command certification. Second, you’ll declare that your drone is airworthy. Then, your drone must meet specific detect-and-avoid performance minimums.

President Trump signed Executive Order 14307 Unleashing Drone Dominance in June of 2025, prompting the FAA to formalize a cohesive rule for BVLOS operations. The FAA published its proposed Part 108 rule in August of 2025. The EO’s 240-day timeline pointed to a final rule around March 2026, but the FAA reopened the comment period in January 2026. Industry observers now expect the final rule in spring 2026, with implementation 6-12 months later

Want to know all the ins and outs of the FAA’s proposed rule? Take a second to watch our Part 108 Explained video.

United States – UTM Systems Mature

The Unmanned Aircraft System Traffic Management (UTM) is “a collaborative ecosystem for safely managing unmanned aircraft (UA or drone) operations at low altitudes.” It is essentially a decentralized digital framework that coordinates airspace management.

UTM will help automate airspace deconfliction and share real-time data with drone pilots and manned aircraft. Air Navigation Service Providers (ADSPs) combine data from ADS-B Out, remote identification, and other sources to help drones safely avoid collisions and integrate into the National Airspace system.

In Phase 4 of UTM development, NASA and the FAA have transitioned from government-led testing to implementation. Private UAS Service Suppliers (USS) will manage airspace coordination across statewide or regional grids. Aloft, for example, provides LAANC flight authorizations and real-time traffic information to drone operators and manned aircraft to ensure safe integration of scalable BVLOS operations.

Global Moves

Governments across the globe are beginning to implement similar BVLOS frameworks in preparation for large-scale automated drone operations.

The European Union Aviation Safety Agency (EASA) continued to flush out U-Space rules. These regulations aim to standardize digital traffic management services, the way UTM is in the United States.

The goal is to facilitate safe BVLOS operations with a cohesive framework for integrating drones into European airspace across member states. Through U-Space, the EASA aims to build investor confidence in drone markets.

In India, the Ministry of Civil Aviation passed the Civil Drone (Promotion and Regulation) Bill 2025. This established a regulatory framework for drone manufacturing, registration, airspace access, and remote identification.

While the bill relaxed import restrictions, it also promoted domestic production and expanded possibilities for commercial drone use in industries like agriculture.

Australia’s Civil Aviation Safety Authority (CASA) launched a massive, year-long BVLOS framework trial. Similar to UTM in the U.S. and U-Space in Europe, the trial aims to streamline and scale automated drone operations in Australian airspace.

United States – FCC Drone Bans

Chinese drone manufacturers produce 70-80% of commercial drones globally. Companies including DJI continue to dominate global market share. Yet, policymakers voiced concerns over Chinese-made drones being used in sensitive situations.

In early 2025, the Federal Communications Commission (FCC) implemented a ban on foreign-made drones listed in its “Covered List,” citing increased national security concerns. While DJI and Autel were the most visible targets, the restriction covers all foreign-produced UAS unless specifically cleared by the Department of War or DHS.

However, the FCC then eased some parts of the ban, exempting drones listed in the Blue UAS Covered List until January 1, 2027. In January, the Commerce Department also dropped plans to implement its own restrictions on Chinese-made drones.

Such flip flopping has increased consumer concern, as well as created regulatory uncertainty for manufacturers and commercial operators.

2026 Compliance Checklist

Flying in the U.S.? This year, you will want to make sure you are still compliant with changing regulations.

The FAA updated a March 2026 deadline for mandatory Remote ID broadcast compliance. Make sure your drone meets Remote ID requirements to avoid fines or operational restrictions.

Register drones weighing more than .55 lbs with FAADroneZone. Your registration number should be visible on the body of the drone.

Stay compliant with VLOS rules until further updates on BVLOS operations under Part 108 are finalized, hopefully by March!

Commercial drone pilots operating under Part 107 rules should also carry insurance. This is typically $1 to $5 million in liability, depending on client, city, and state-specific requirements.

Adding hull insurance can further protect operators by covering physical damage to the drone itself, helping mitigate financial loss from crashes, theft, or equipment failures.

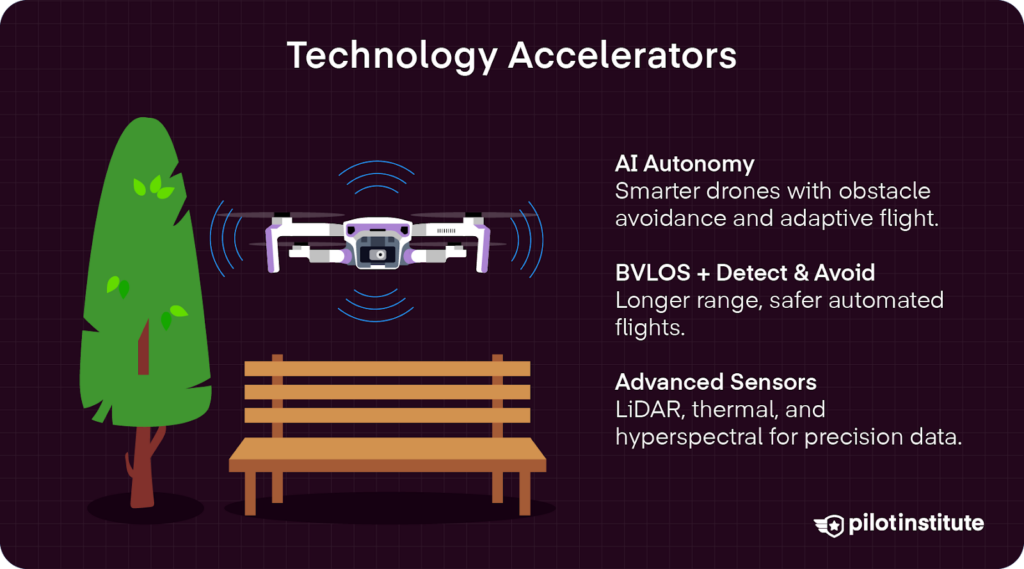

Technology Accelerators

AI-Powered Autonomy

AI systems use reinforcement learning (RL) models to learn optimal behaviors when interacting with their environment. Constant feedback on performance outcomes helps adjust future decisions for safer, more reliable drone automation.

Popular RL algorithms include Deep Q-Network methods, which are valued for their strong obstacle avoidance performance.

RL models are experiencing rapid advancements, allowing automated drones to better navigate complex airspace, optimize flight paths, and avoid obstacles. They can adapt to changing environmental conditions with minimal human interventions.

BVLOS & Detect-and-Avoid

Range extensions only possible in BVLOS operations allow drones to cover significantly more ground than traditional VLOS patrols. At the same time, operating costs drop significantly with less need for constant human control and ground crews.

Sensor fusion packages combine ADS-B, optical flow, and millimeter-wave radar. These systems allow drones to safely navigate complex environments with minimal human supervision.

Detect-and-avoid systems will play a major role in Part 108 operations, allowing for safer BVLOS flights.

Sensor & Payload Revolution

In 2026, lightweight, high-performance sensor and payload systems are becoming the norm. Top options include solid-state LiDAR units with ±3 cm accuracy that are only around 2 lbs (1 kg). These systems utilize 640×512 thermal cores capable of detecting temperature differences as small as ≤50 mK.

Pushbroom hyperspectral pods covering 900-1,700 nm enable rapid collection of spectral data for applications like crop analysis, mineral mapping, and environmental monitoring.

Industry Adoption Trends

Energy & Utilities (14.5% CAGR)

The energy and utilities sector is experiencing rapid growth, with drones expanding at an impressive 14.5% CAGR from 2025 to 2033.

FAA-approved Shielded Corridors will enable safer and more efficient transmission line inspections. Considering the high cost of helicopter or human climbing inspections, drones offer incredible cost savings.

Additionally, hydrogen-powered VTOL drones like Bluebird Aero System’s WanderB-VTOL are also being used for longer transmission patrols. Extended flight endurance of up to six hours allows for more comprehensive infrastructure monitoring with far fewer risks.

Logistics & Delivery

In 2026, the delivery drone market is expected to reach $1.47 billion. By 2031, that growth should hit $6.74 billion, showing a 35.69% CAGR.

Currently, Zipline’s P2 drop-pods are a favorite for effectively distributing medical supplies to hard-to-reach areas. The P2 models can carry nearly double what the P1 model could, offering Michigan Medicine impressive delivery capabilities.

However, with the implementation of Part 108, many retailers are investing in automated drone delivery networks. Companies like Wing continue to expand their urban networks, offering Walmart expanded delivery potential.

Take for example, Wing’s expanding Dallas-Fort Worth metro network, covering thousands of homes and delivering Walmart orders in less than 30 minutes. In 2027, Wing plans to move into the Atlanta metro area as well.

Agriculture & Environmental

The agricultural and environmental sector has enjoyed more complex multispectral sensors to generate Normalized Difference Vegetation Index (NDVI maps). Such data provides farmers with actionable insights on crop health, irrigation needs, and nutrient management.

Unfortunately, the climate-smart pilot programs implemented by the U.S. Department of Agriculture under the Biden Administration has been axed. The $3.1 billion program was canceled in April of 2025, citing “sky-high administration fees” that “often provided less than half of the federal funding directly to farmers.”

Construction & Infrastructure

In construction and infrastructure, drones are increasingly being used for volumetric stockpile analysis. Using LiDAR and photogrammetry, 3D models built on aerial imagery data can help calculate volumes of certain stockpiled materials on the ground.

Data can be directly exported to CAD software for seamless integration into project workflows. Real-time, accurate calculations vastly improve inventory management and save money in work hours and incorrect supply planning.

Take the example of the firm Ninyo & Moore’s use of a DJI Phantom 4 Pro equipped with photogrammetry software to stitch together thousands of high-resolution pictures into 3D models offering accurate measurements of stockpiled materials.

Public Safety & Defense

Public safety and defense is continuing to see strong growth. In late 2025, the Department of Defense pledged to purchase 1 million drones from 2027 to 2028. To meet the increase in demand, AeroVironment is scaling production with the expansion of its Switchblade factory in Utah.

At the local level, police and fire agencies are increasingly deploying tethered drones for 24/7 aerial surveillance to ensure rapid response to emergencies and public safety needs.

Media, Survey, Insurance

Increasing price compression poses a risk as media, survey, and insurance markets become more standardized.

Operators in this sector are trying to stay competitive by differentiating their services. Many now offer high-resolution orthomosaic mapping for distortion-free accuracy.

Some insurance and roofing companies are also offering AI-powered hail-damage detection to automate roof inspections. Drones help reduce costs and safety risks associated with roof inspections.

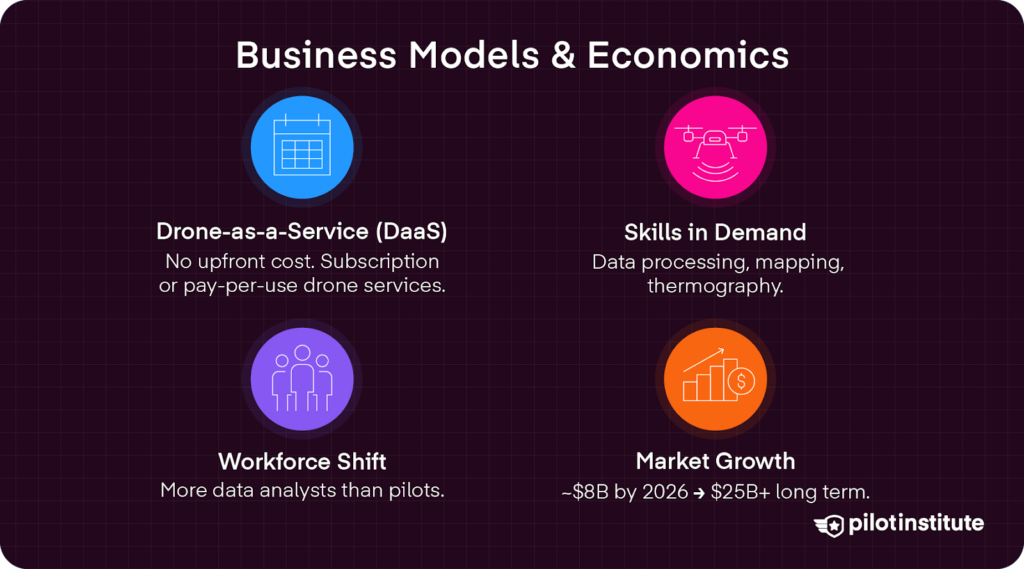

Business Models & Economics

Drone-as-a-Service (DaaS)

With DaaS, businesses can avoid purchasing expensive equipment outright. Instead, they can access the latest drone technology and professional expertise on demand.

Providers like AeroVironment and ZenaTech offer companies an affordable way to scale drone operations. They offer subscription or pay-as-you-go models in industries from inspection to agriculture.

ZenaTech is a top leader in the field, with 23 DaaS locations serving government and corporate clients. The company offers several subscription tiers giving clients access to complex tech, like multispectral sensors and advanced AI automation. Higher tiers also include data capture, processing, and actionable insights.

The DaaS market is growing rapidly. Nasdaq reported that it is expected to reach $8 billion by the end of 2026, “with longer-term forecasts suggesting expansion toward $25 billion+ over the next decade as adoption accelerates across commercial and government sectors.”

Workforce & Skills Gap

With the coming of Part 108 comes new roles in drone operations. By 2027, demand will include nearly three times as many data analysts as pilots. In fact, the drone analytics market is expected to reach $6.5 billion by 2027 thanks to increasing demand for processing aerial data related to autonomous flight operations.

The need for professionals who can process and interpret such complex data is growing, but there is a skill gap to overcome in the short-term. Certifications for ArcGIS Pro, Level-I Thermography, and Pix4d Mapper are becoming increasingly important to stay competitive.

Security, Privacy & Counter-UAS

U.S. Drone Makers Seek Asian Markets

The U.S. is not the only nation concerned about Chinese drones. In response, American drone makers are looking to expand into Asian markets, according to a report from Reuters.

Several American drone manufacturers displayed their latest models at the Singapore Airshow in February 2026. Their goal was to “expand their business beyond the Pentagon to countries in Asia that are increasingly concerned about the threat posed by China’s military buildup.”

American manufacturers of military-grade drones are courting Asian governments in Singapore, Taiwan, the Philippines, South Korea, and Japan. Shield AI, for example, displayed its V-BAT reconnaissance and surveillance drone at a hefty price tag of $1 million a piece.

Even old-school defense companies are looking to get in on the action. Looking beyond the Pentagon, Boeing, General Atomics, Lockheed Martin, and Northrop Grumman are also developing Collaborative Combat Aircraft (CCA), or “fighter-jet drones designed to fly alongside next-generation manned fighters.”

Counter-UAS (CUAS) Market Growth

As threats from unauthorized drones continue to grow, the Counter-UAS industry is adapting. Advanced drone detection is more efficient using multi-sensor fusion stacks that combine radar, RF, and Electro-Optical/Infrared technologies.

The recent Hoverfly/AeroVironment partnership now offers tethered radar pickets for continuous coverage. This offers a scalable solution for security and defense.

Data Governance

Data governance is critical for managing sensitive infrastructure data in drone operations. FedRAMP Moderate sets a framework for managing non-public, sensitive data. Aerial data collected using video, LiDAR, and flight telemetry is managed over a certified cloud system. This uses robust security protocols required by FedRAMP authorization.

On-premises solutions like DJI’s FlightHub 2 offer sensitive data management locally, without risks associated with handling data through the cloud.

Both approaches utilize end-to-end AES-256 encryption, role-based access, and zero-trust APIs for verification to ensure that only authorized, authenticated users can access sensitive data.

Challenges & Risk Factors

Given the rapid pace of technological advancements, there is a risk of regulatory lag. FAA regulations must keep up with the technology.

State laws also need to avoid conflicting with federal supremacy over airspace regulations as the situation continues to evolve.

Additionally, complying with the National Defense Authorization Act (NDAA) can be expensive. NDAA compliance requires all layers of the supply chain to avoid certain Chinese manufacturers, like Huawei. This has led to a push for Western equipment manufacturers, which could force higher costs on consumers.

As Part 108 invites more automated drones to America’s airspace, there is also the obvious risk of increased airspace congestion and noise pollution in areas served by BVLOS drone delivery operations.

Even more concerning, NASA’s Urban Air Mobility maps identified potential BVLOS flight paths as intersecting with low-altitude helicopter emergency medical services (EMS) routes.

Research from cities like Dallas shows the 400 to 600 feet AGL corridors carved out for BVLOS traffic could interfere with EMS operations, which often occur under 500 feet AGL.

This highlights the need for robust detect-and-avoid technologies to prevent incidents with manned aircraft.

Beyond 2026 – Future Trends to Look For

Swarming & Collaborative UAS

Drone swarm technologies are advancing rapidly with programs including DARPA OFFSET. The software can coordinate drone swarms of up to 250 drones operating simultaneously. While primarily for military applications, swarming software is also being adapted to deal with cargo hub security in civilian use settings.

Hydrogen & Hybrid-eVTOL Cargo

Hydrogen and hybrid-electric VTOL aircraft will transform cargo logistics. The Hydrogen & Electric drone market is expected to reach $617.7 million in 2026. Yet, strong growth in the upcoming years promises to accelerate adoption of longer-endurance platforms that can carry heavier payload capacities. This will ultimately expand regional freight corridors and delivery networks worldwide.

These drones offer extended flight ranges, reduced emissions, and rapid vertical takeoff and landing capabilities. Projects such as Amazon’s Cargoport aim to leverage autonomous eVTOL drones to vastly improve the speed and efficiency of delivery services.

Market Projection Chart

Conclusion

In 2026, success in the drone industry means tracking the regulatory changes, staying ahead of AI advances, and leveraging data-centric operational models.

Drone operators should take concrete steps now to ensure compliance in a changing environment. You can audit your fleet for Remote ID compliance and upskill pilots to take on data analyst roles. Furthermore, engage with UTM providers to integrate your operations into managed airspace systems.

Looking forward, competitiveness will be defined by who has the best data. By 2030, drone operations will process terabytes of data to make actionable decisions in seconds. Will you be ready?